Volatility is starting to creep back into the markets. It’s not obvious from the 30,000-foot view, but a few corners of the global markets are becoming jittery. Exhibit A: US real estate investment trusts (REITs), which tumbled sharply in recent sessions, presumably on the fear that this interest-rate sensitive asset class is vulnerable if the Fed is getting close to hiking interest rates.

One thing hasn’t changed: US stocks remain in the lead in absolute and relative terms among the major asset classes, based on the trailing 250 trading-day total return (a rough proxy for one-year performance) via our usual set of proxy ETFs. Volatility is also inching higher for US equities, although on the margins and from a low base. In any case, with stocks sitting on handsome gains, no one’s losing sleep over slightly higher equity vol.

US equities (VTI) are ahead by 17.3% for the 250 trading days through yesterday (September 16). If there’s such a thing as a resilient investment these days, the US stock market qualifies.

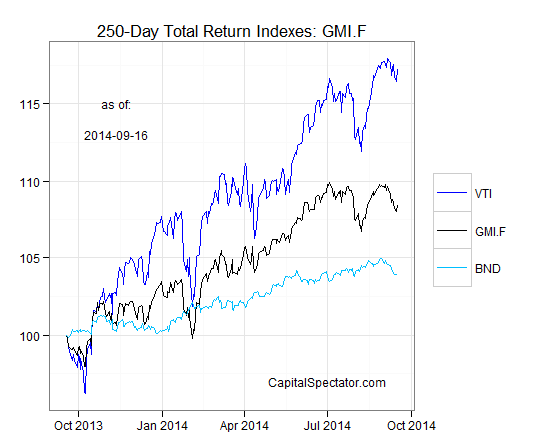

For a graphical recap, consider the relative performance histories for each of the major asset classes for the past 250 trading days by way of the ETF proxies. The chart below shows the performance records through September 16, 2014, with all the ETFs rebased to 100 using a start date of September 18, 2013:

Next, let’s review an ETF-based version of an unmanaged, market-value-weighted mix of all the major asset classes–the Global Market Index Fund, or GMI.F, which is comprised of all the ETFs in the table above. Here’s how GMI.F stacks up for the past 250 trading days through September 16, 2014. This investable strategy is up 8.5% over that period, or roughly midway between the returns for US stocks (VTI) and US bonds (BND).

Comparing the overall dispersion of returns for the major asset classes via ETFs suggests that the rebalancing opportunity is quite low for GMI.F vs. recent history. The dispersion of 250-day returns for our set of ETF proxies has fallen lately, dipping to the lowest level in recent history. Analyzing the components of GMI.F with a rolling median absolute deviation based on one-year returns for the ETFs–the GMI.F Rebalancing Opportunity Index, as it’s labeled on these pages–suggests that there’s relatively lower potential generally for adding value by reweighting this portfolio in comparison with the previous months of this year. Keep in mind that the opportunity for productive rebalancing will vary depending on the choice of holdings and historical time window. Meantime, don’t overlook the possibility that any given pair of ETFs may present a substantially greater or lesser degree of rebalancing opportunity vs. analyzing GMI.F’s components collectively.

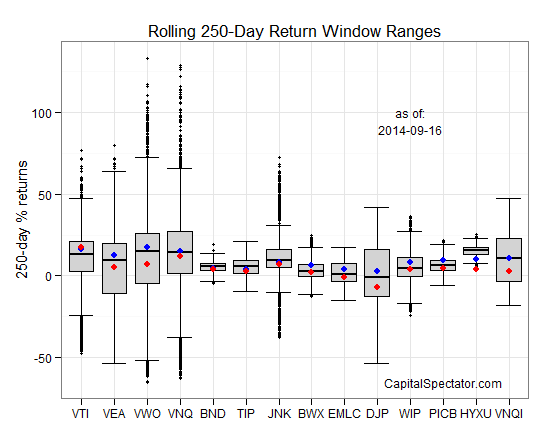

Finally, let’s compare the rolling 1-year returns (250-trading-day performance) for the ETFs in GMI.F via boxplots for a revealing comparison of price momentum. The gray boxes in the chart below reflect the middle range of historical 250-day returns for each ETF—i.e., the 25th to 75th return percentiles. The red dots show the current return (as of Sep 16) vs. the 250-day return from 30 trading days earlier (blue dots, which may be hiding behind the red dots in some cases). As you can see, the strong upward bias in performance has faded lately for several asset classes.

The ETF Asset Class Performance Review, which offers a deeper look

at an ETF-based view of asset classes. For more information and a

recent sample, see CapitalSpectator.com/premium.

Pingback: Wednesday links: unique life experiences | Abnormal Returns