Recession forecasts are topical lately, driven by the recent inversion of the Treasury yield curve for 2- and 10-year rates. But some economists see a strong labor market as a key factor that will keep the expansion alive.

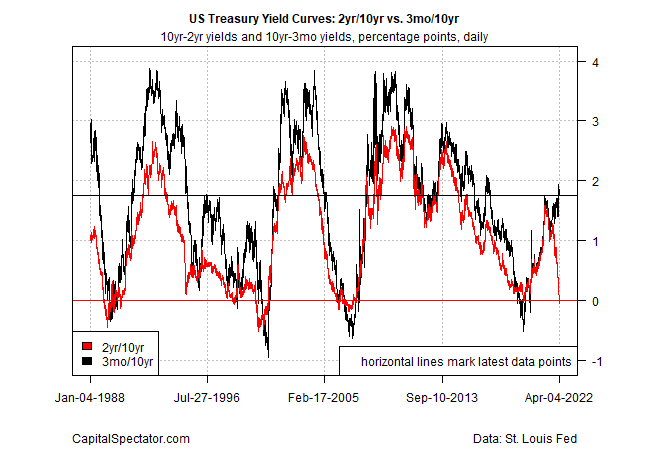

Let’s start with the dark side. The 2yr/10yr yield spread inverted recently, triggering a forecast that a US recession is a high probability at some point in the months ahead. “Historically, the yield curve inversion has meant that the fuse is lit for a recession. But the timing of a recession is impossible to predict at this stage,” says Mark Hackett, chief investment of research at Nationwide.

One reason for thinking the 2yr/10yr warning is premature and perhaps wrong: the 3mo/10yr spread, which is arguably a more reliable indicator of business-cycle risk, remains positive by a wide degree and is effectively pricing in growth for the near term.

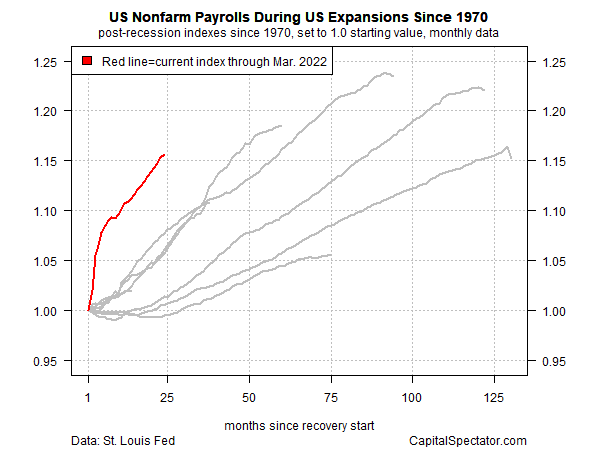

Another factor to consider: the labor market continues to expand at a healthy pace. US nonfarm payrolls rose 431,000 in March, extending a run of healthy gains that suggests the economy’s forward momentum remains strong. Comparing the labor market’s recovery since the coronavirus recession ended nearly a year ago with previous cycles highlights the power of the current hiring spree.

“I just don’t see what would cause businesses to do a complete 180 and go from ‘We need to hire all these people and we can’t find them’ to ‘We have to lay people off,’” says Aneta Markowska, chief economist for Jefferies, an investment bank.

Goldman Sachs estimates that the US labor market is the tightest since World War II. Demand for employees exceeds supply by more than 5 million, marking “the most overheated level of the postwar period both in absolute terms and relative to the population,” advises Jan Hatzius, Goldman’s chief economist, in a research note this week.

The tight conditions aren’t without risks. As Hatzius explains, “In order to reduce wage pressure to levels at least broadly consistent with the Fed’s inflation target, we estimate that the [labor market] gap needs to shrink by at least one-half.”

Therein lies a possible path that could lead to recession via the Federal Reserve increasingly focuses on inflation, which remains elevated and appears unlikely to fall in the immediate future. As the central bank tightens monetary policy to cool pricing pressure, the squeeze could go too far and take a bite out of the labor market and the economy overall.

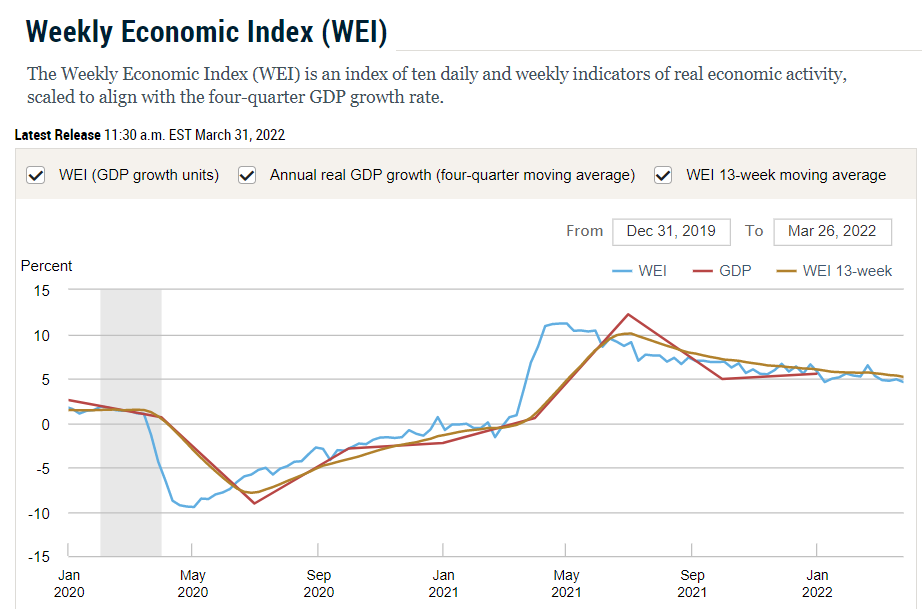

The future, in short, is uncertain, as always. For now, however, recession risk remains low. The New York Fed’s Weekly Economic Index, a multi-factor measure of current economic activity, continues to reflect a robust expansion through the end of March.

Economic momentum could fade, of course, and perhaps quickly. The risk of trouble is more than trivial at a time when blowback from the ongoing war in Ukraine is roiling the global economy on multiple fronts.

“I don’t think we’re going to go into a recession in the next 12 months,” predicts Megan Greene, a senior fellow at Harvard’s Kennedy School and the Kroll Institute’s global chief economist. “I think it’s possible in the 12 months after that.”

That’s always true, of course. The only thing that’s clear today is that the economy continues to expand at a solid pace and the odds are low that a recession will start in the immediate future. Looking beyond the next month or two, by comparison, is highly uncertain – and it always will be.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report