The Federal Reserve left interest rates unchanged yesterday, as widely expected. But the possibility of a hike in June is lurking… maybe. “This latest [FOMC] statement has not laid out a strong position for a June rate hike,” Bill Irving, a Fidelity portfolio manager, tells Reuters. Meanwhile, the Treasury market is sending mixed signals. On the one hand, yields ticked lower, perhaps in anticipation of a weak first-quarter GDP report that’s due later today. But then there’s the sight of the Treasury market’s inflation expectations rising to the highest levels since last summer. It all adds up to a strange brew of market signals.

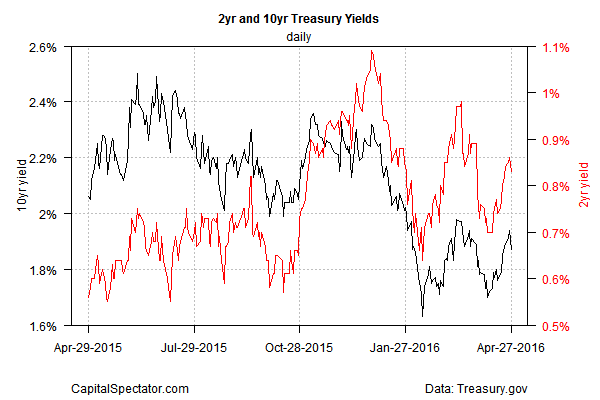

Note that the 2-year yield (considered the most sensitive for rate expectations) dipped yesterday (Apr. 27), as did the benchmark 10-year yield, based on daily data via Treasury.gov. Both rates seem to be stuck in a holding pattern of middling yields relative to recent history. In short, not a lot going on here.

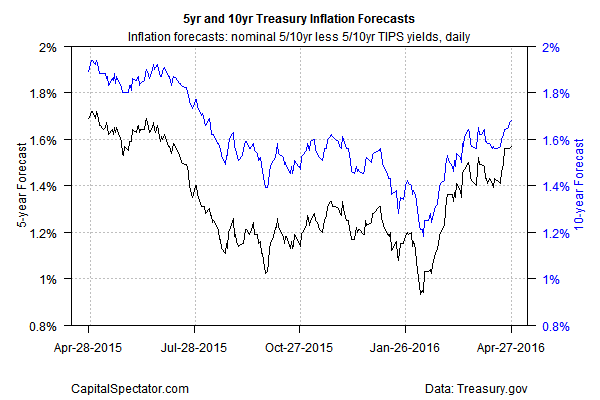

It’s another story with the Treasury market’s implied inflation forecasts—nominal yields less the inflation-indexed counterparts. For instance, the 10-year maturities are now projecting inflation at 1.68%–the highest since last August. That’s a strange sight if the crowd is right about today’s first look at the Q1 GDP report, which is on track to stumble to its slowest pace in a year. The Altanta Fed’s GDPNow model, for instance, is estimating that US output in the first three months of this year will stumble to a tepid 0.6% (seasonally adjusted annual rate)–less than half the already sluggish 1.4% pace in last year’s Q4. Slower growth and higher inflation? Hmmm.

One analyst thinks that recent increase in the market’s inflation outlook is partly due to correcting for previous extremes on the downside in early 2016. “We took inflation expectations too low as we flinched against possible declines in oil,” notes Jim Vogel, head of interest-rate strategy at FTN Financial. “Now we have to take inflation expectations back up and find where there’s equilibrium.”

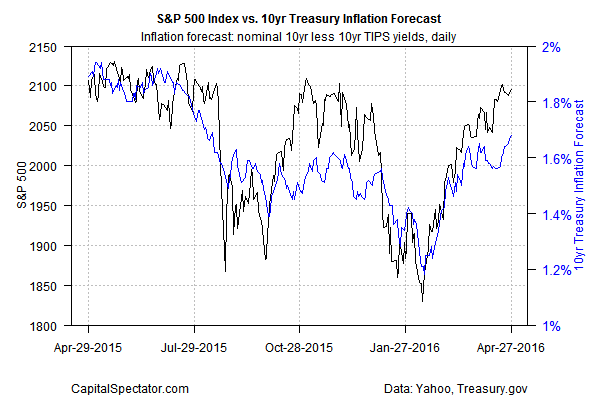

Whatever the reason, the stock market seems to like firmer inflation estimates… for now. In a world that’s still struggling to overcome deflation risk and slow growth, the possibility that pricing pressures are ticking higher in the US offers a degree of encouragement. Note the tight correlation over the past year between the implied inflation outlook via the 10-year maturities and the S&P 500 in the chart below. By this standard, the recent revival in the market’s expectation for inflation is a factor that’s boosting equity prices.

By this logic, one might wonder if a sharply softer GDP report today is a clue that the recent rise in the market’s inflation estimate is headed for reversal of fortunes. The alternative view is that today’s Q1 GDP data will deliver sound and fury on the downside that signifies nothing about the second quarter and beyond.

The upbeat narrative certainly finds support in the recent rise inflation expectations and the stock market. The acid test, for good or ill, arrives in next week’s April update on US payrolls.