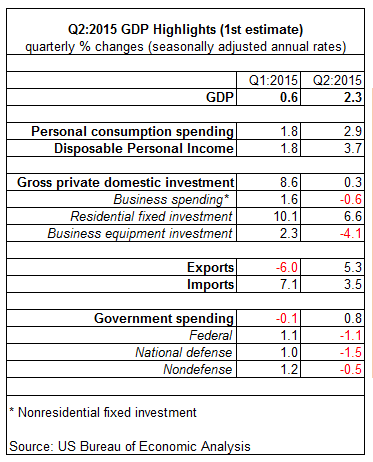

The US economy revived in this year’s second quarter, according to today’s preliminary GDP estimate from the government. The 2.3% increase in output in Q2 vs. the previous quarter (real seasonally adjusted annual rate) is a modest pace, although the advance offers an encouraging improvement over Q1’s tepid 0.6% rise.

Stronger consumer spending and exports provided most of the heavy lifting in terms of the rebound. Growth in disposable personal income also accelerated in Q2, suggesting that consumption may strengthen in the months ahead. By contrast, business spending (nonresidential fixed investment) weakened, dipping into the red for the first time in three years.

“I think it’s an O.K. performance. Underlying growth is stable but not spectacular,” advises Nariman Behravesh, chief economist at IHS. “The economy is plodding along.”

Although today’s numbers reflect an economy that’s growing only modestly (some might say sluggishly), there’s enough upside momentum to keep the possibility alive that the Federal Reserve may start raising interest rates in September.

“The second-quarter US GDP data support the Fed’s more upbeat tone on economic conditions and suggests that the economy could cope with higher interest rates,” according to Steve Murphy, US economist at Capital Economics.

At the very least, today’s update supports the view that the economy is in no imminent danger of sliding into a new recession. Although some bearish analysts have been warning recently that growth was stalling, The Capital Spectator’s business-cycle reviews have suggested otherwise in recent months—see here, for instance. The Q2 GDP data effectively confirm that the macro trend remains positive and picking up speed relative to Q1.

Is the acceleration in growth sufficient to convince the central bank to roll out the first rate hike since 2006 at the September FOMC meeting? Perhaps, although much depends on how the incoming numbers stack up in the weeks ahead, starting with next week’s July report on nonfarm payrolls.

Meantime, the Fed is in a slightly more hawkish mood, according to economist Tim Duy. Although the central bank’s latest commentary contained subtle changes, “I would count it was somewhat more hawkish as the Fed gears up to hike rates later this year,” Duy reasoned. “By no means, however, did the statement make any definitive signal about September.”

Are the signals about to become more definitive, one way or the other? Next week’s reports may offer a telling clue.