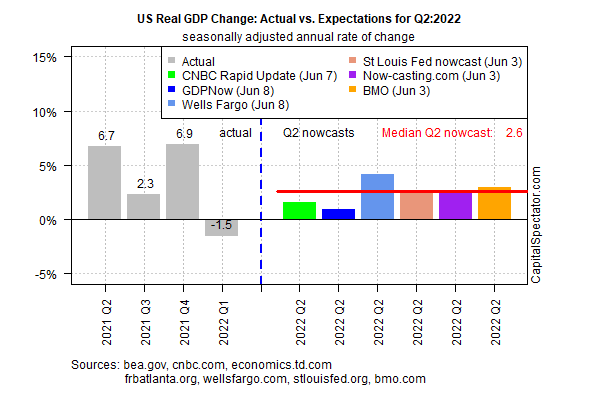

Recession talk has spread like Covid recently, but next month’s initial estimate of US economic activity for the second quarter remains on track to post a robust rebound after Q1’s loss, based on a set of nowcasts.

US gross domestic produc (GDP) is projected to rise 2.6% in the “advance” estimate scheduled for release on July 28 from the Bureau of Economic Analysis. This estimate is based on the median of several Q2 nowcasts compiled by CapitalSpectator.com.

Using the median as a guide indicates that today’s revised outlook is unchanged from the previous estimate, published on May 26.

Encouraging, but there are several risks to keep in mind — risks that could derail today’s upbeat outlook, including the ongoing Ukraine war, high inflation and rising interest rates. But for the moment, the US economy appears relatively resilient, a point noted in last week’s update of PMI survey data that estimate US business activity.

“The S&P Global US Composite PMI Output Index posted 53.6 in May, down from 56.0 in April, to signal a solid but slower upturn in private sector business activity,” advises S&P Global Market Intelligence. Any reading above the neutral 50 mark indicates growth. “The softer rise in output reflected slower increases in the manufacturing and service sectors, amid hikes in selling prices and supply-chain disruption.”

The key question is whether the June economic profile will deteriorate further, and drag down the final round of Q2 GDP estimates? That’s a non-zero possibility, although several early estimates for this month still point to a growth bias. Notably, the labor market remains tight and jobless claims are low, suggesting that payrolls – a key component for the economy – will provide stability through the end of this month and beyond.

Nonetheless, a recent survey reveals that “Americans are deeply pessimistic about the US economy,” which may become a self-fulfilling prophecy for economic activity in the second-half of the year.

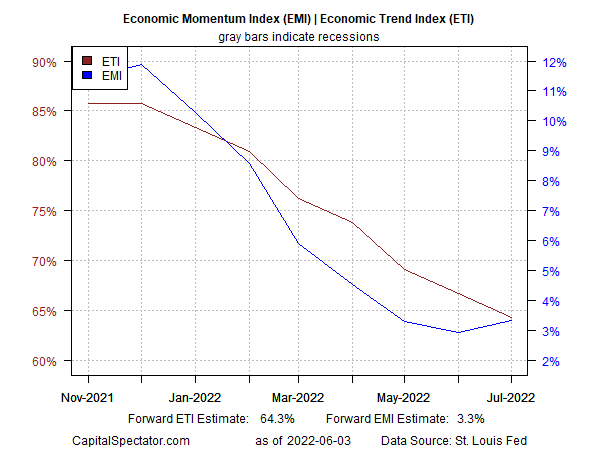

But at this late date in the current quarter, the odds look favorable for a bounce of some degree in GDP for Q2. Given the state of the world at the moment, however, confidence is unusually low about what follows in Q3. As noted in this week’s update of The US Business Cycle Risk Report, US growth is still decelerating, based on a set of proprietary indicators (see chart below).

The good news: there’s a hint that the growth slide may be stabilizing. Using forward estimates for the two multi-factor business-cycle indexes in the chart above highlights that EMI (blue line) is showing a slight recovery for July. It’s premature to cite this as a high-confidence signal that Q3 growth will hold up, but it’s also too early to dismiss the possibility.

The next several weeks of incoming data, in other words, may be crucial for deciding if the expected Q2 rebound will carry over (or not) into Q3.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report