The ongoing bear market in Treasury bonds is among the worst on record, but several sectors of the fixed-income market remain ports in a storm, based on year-to-date results through Thursday (Oct. 5) for a set of fixed-income ETFs.

“Bonds maturing in 10 years or more have slumped 46% since peaking in March 2020,” Bloomberg reports. “Compared with previous bond-market meltdowns, long-term Treasuries are seeing one of the most extreme undoings in history. The losses are over twice as big as those seen in 1981 when 10-year yields neared 16%.”

“It’s quite something,” observes Thomas di Galoma, co-head of global rates trading at BTIG. “To be honest with you, I had never thought I would see 5% 10-year notes ever again. We got caught in an environment post global financial crisis where everybody just thought rates were going to remain low.”

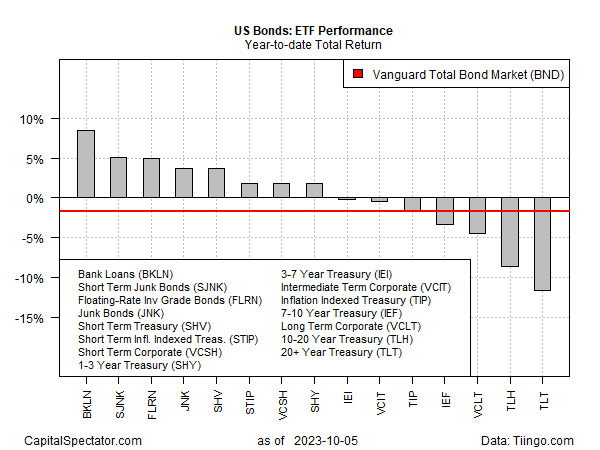

Despite the bearish tailwinds blowing through the market, it’s not an across-the-board rout via a set of ETF proxies. Notably, a portfolio of bank loans (BKLN) is leading the field with a solid 8.5% return so far in 2023 through yesterday’s close (Oct. 5). Tied for second place this year: moderate gains of roughly 5% each for short-term junk bonds (SJNK) and floating-rate notes (FLRN).

The steepest losses in the bond market in 2023 are concentrated in long maturities, led by the near-12% slide in iShares 20+ Year Treasury Bond ETF (TLT).

When will the pain end for longer-dated bonds? The answer is tightly linked to how the Federal Reserve’s monetary policy evolves in the months ahead.

San Francisco Fed President Mary Daly dropped a tantalizing clue in a speech yesterday, advising that if the recent rise in Treasury yields persists, the central bank may no longer need to raise interest rates.

“The bond market has tightened quite considerably over about 36 basis points since we met in September,” she said at the Economic Club of New York on Thursday (Oct. 5). “That is equivalent to about a rate hike. So then the need to do tightening additionally is not there.”

The Fed funds futures market is currently estimating a moderately high probability that the Fed will leaves its target rate unchanged at the next policy meeting on Nov. 1.

Perhaps the crucial factor for assessing the path ahead for monetary policy is the degree of economic resilience, or the lack thereof, going forward. “It’s a bond market selling off because of an underlying macro resilience and we see that in higher real rates,” notes Padhraic Garvey, managing director at ING.

There are signs that the recent rebound in US economic activity may be peaking. If so, that could create new headwinds for stocks, but it would likely bring a reprieve for long-dated Treasuries, which tend to rally when the economy stumbles.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report