The resonance of summer warnings that the US economy is on the precipice of recession continue to fade from the perspective of the upcoming third-quarter GDP report. The latest run of numbers continues to highlight encouraging nowcasts for the government’s initial Q3 report, scheduled for release on Oct. 30.

There’s still a month to go before the official estimate is released, which means that a lot could happen in October to derail the upbeat outlook. But according to current GDP nowcasts, the odds still favor expectations that output will rise at a moderate pace.

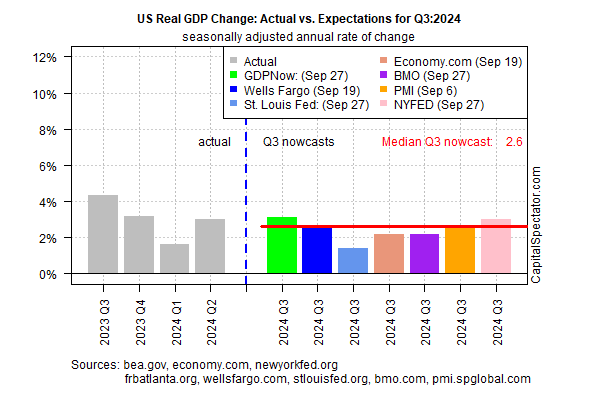

GDP is on track to increase at a 2.6% real annualized rate in Q3 via today’s revised median nowcast, based on several estimates compiled by CapitalSpectator.com. That’s modestly below Q2’s strong 3.0% rise, but a mid-2% advance, if correct, renders recession risk null and void for the third quarter.

Today’s 2.6% nowcast is unchanged from the previous update on Sep. 20. In fact, median nowcast updates over the past month have been relatively steady in the low- to mid-2% range, an encouraging sign for expecting ongoing growth in Q3. In late-August, for instance, we wrote: “If a recession in the US has started, or is imminent, the threat has yet to show up in the latest run of nowcasts for third-quarter GDP.”

Recession forecasters, however, remain convinced that the economy is set to contract. The only difference from the summer warnings is that the expected start date, once again, has been pushed forward.

“The clock is ticking and we are in black swan territory,” warns Mark Spitznagel, chief investment officer and founder of Universa. “The clock really starts when the [Treasury yield] curve disinverts, and we’re here now.”

BCA Research advises that a US recession remains the “most likely outcome.”

Perhaps the fourth quarter will finally prove the pessimists right. Meanwhile, the regular nowcasting updates on these pages strongly indicates that an NBER-defined recession hasn’t started in Q3.

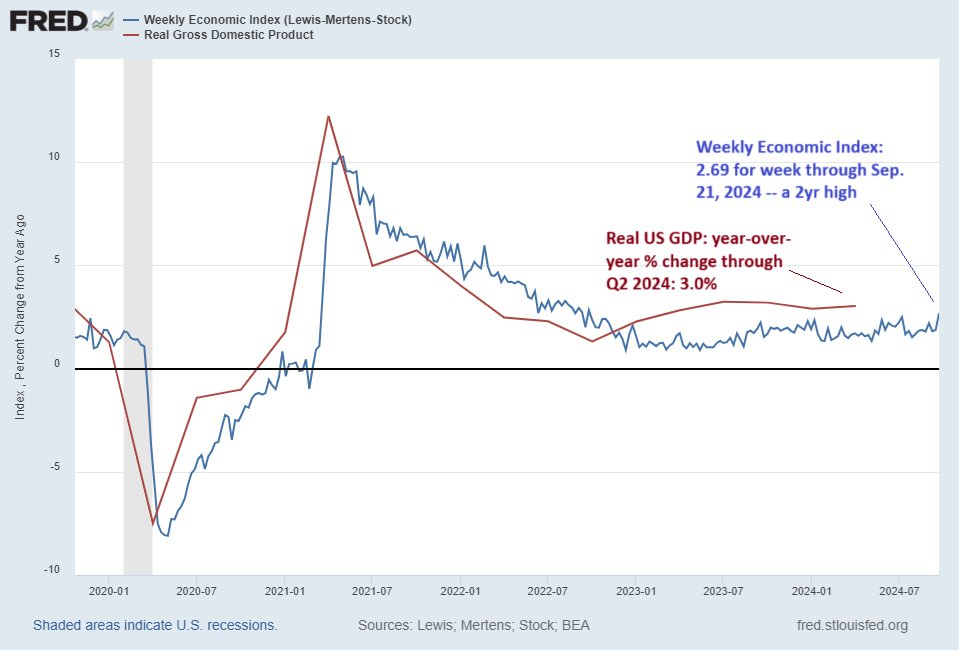

Early estimates for October, via this week’s update of The US Business Cycle Risk Report, tell a similar story. In fact, forward estimates for a pair of proprietary business-cycle indicators suggest that economic activity is rebounding after the recent soft patch. The current update of the Dallas Fed’s Weekly Economic Index aligns with that view — this multi-factor benchmark rose to a two-year high for the week through Sep. 21.

Betting that a new recession is imminent, in short, still comes with long odds, based on a wide variety of indicators.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report