It’s old news that’s forever relevant: rebalancing is the worst choice for managing risk… except when compared with everything else. Granted, it’s not a silver bullet (nothing is) and in the hands of an amateur it can lead to trouble. But when paired with a reasonable asset allocation and a schedule of periodically resetting weights, rebalancing remains the first choice for managing portfolio risk.

This year’s roller-coaster ride in financial markets offers the latest test, Morningstar reminds. “Rebalancing your portfolio is one of those beneficial habits–like flossing every day or dusting under the refrigerator–that’s easy to let slide,” the investment consultancy advised in an updated review of the strategy. “But if your portfolio’s equity exposure crept up over the past few years, the sudden market correction in February and March was a harsh reminder of why it’s a good idea.”

Unless you’re a dedicated buy-and-holder for the long run (a rare bird), a rebalancing plan is, when you get right down to it, the only game in town. The details matter, of course… a lot. Once you’ve made the easy and eminently wise decision to rebalance, the hard work begins, namely: How and when to rebalance?

The possibilities are endless, and within the range of options lie many traps and dead-ends. But there’s also a fair amount of opportunity. Overall, navigating the choices may be the most important investment decision you make (after prudently choosing asset classes and proxy investments to populate your asset allocation plan).

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

The good news: effective rebalancing doesn’t have to be complicated or sophisticated. A simple plan to reset weights on a regular or even irregular schedule can do quite a lot of the heavy lifting. But it’s important to manage expectations in this corner. Although some forms of rebalancing may boost the odds of earning a higher return in the long run over a buy-and-hold methodology, most of the benefits from rebalancing will likely come from risk management.

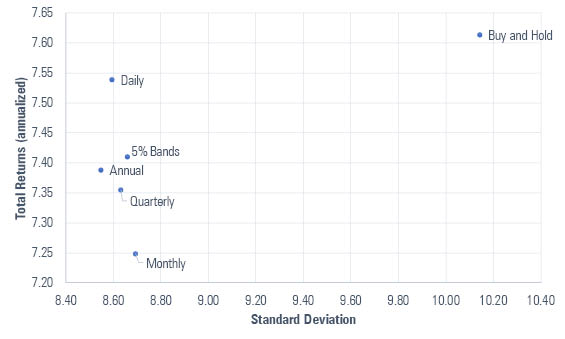

As an illustration, the recent Morningstar article reviews results for a simple 60%/40% stock/bond portfolio. For the trailing 15-year period through this past May 31, for example, it’s instructive to consider how a buy-and-hold version of the strategy fared against several flavors of rebalancing from a risk (return volatility) and performance perspective.

As the following chart shows, rebalancing for this simple example came with a price tag in the form of modestly lower return. But the reduction in performance is also associated with a considerably bigger drop in risk (volatility). The buy-and-hold portfolio earned 7.61% a year with a near 10.2% annualized standard deviation. Several different rebalancing frequencies trimmed the return slightly (roughly 7.25% to 7.55%). Note the larger reduction in risk – from about 10.2 to under 8.8.

The risk-return trade-off, in other words, looks favorable for some level of rebalancing. To be sure, this basic example doesn’t show a dramatic decline in risk. In this year’s dramatic correction, for example, plain-vanilla rebalancing strategies probably reduced volatility only modestly.

But simple, calendar rebalancing strategies can be enhanced. The devil’s in the details, of course, and it’s easy to fall into the trap of thinking that there’s an easy solution to avoiding the deepest market drawdowns without sacrificing return. But with careful research and testing, there are opportunities for enhancing standard rebalancing strategies.

Shifting the odds of success in your favor starts with carefully choosing the opportunity set from the broad-brush realm of the major asset classes. Will you add alternative asset classes and alternative strategies to the mix? How granular will go in your choice of standard assets classes? Which funds will you use to represent those choices? Will it be index funds? Actively run products? A mix of both? Will you also use individual securities?

Once you have a short list of investments, you’ll need a strategy for deciding how and when to rebalance. This is the most challenging aspect of rebalancing-strategy design lies. Fortunately, there’s a deep and wide research pool to draw on to avoid the obvious mistakes and focus on the more-compelling opportunities.

Ultimately, it’s essential to manage expectations. The idea that you’re going to double the Sharpe ratio without materially reducing return, or substantially ramp up performance with little or no commensurate increase in risk in some form is naïve. But you can make quite a bit of progress in enhancing simple rebalancing strategies, assuming your research process is prudent and systematic rather than ad-hoc and subjective.

Every rebalancing strategy should also be customized to match various facets of risk expectations and investment objectives. Yes, it’s a lot of work. But there’s really no other choice if you’re not willing to live with Mr. Market’s hands-off asset allocation and rebalancing approach.

If you’re not sure where to begin, start with a simple baseline. Vanguard suggests a reasonable starting point: “Check your portfolio at least once a year, and if your mix is off by at least 5 percentage points, consider rebalancing.”

Should do more? Maybe, but maybe not. There are no one-size-fits-all answers because every investor is different. Meantime, consider a robust reference point: owning a proxy of the global market portfolio and letting it ride is, in theory, the optimal portfolio for the average investor with an infinite time horizon. The first question: How you differ from that profile and what are the rebalancing and asset allocation implications?

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Pingback: Rebalancing Is a Strategy for Managing Risk - TradingGods.net

It is said that Claude Shannon rebalanced his portfolio daily. Looks like he was correct .