Inflation has probably peaked. The problem is that the slide from the peak is proving to be slower than expected, dipping at a glacial pace, if any, depending on the metric. Inflation persistence, in other words, is increasingly the new new worry.

Yesterday’s August update on US consumer inflation certainly highlights the persistence risk. Economists were looking for a decline in the annual rate of headline CPI to 8.1%, based on Econoday.com’s consensus forecast. The actual decline was milder, dipping to 8.3% from July’s 8.5% increase. Better, but hardly inspiring for thinking that pricing pressure is fading in a meaningful degree. More worrisome: core CPI, generally a more reliable forecast of the trend, ticked up last month.

The hotter-than-expected report triggered new forecasts that the Federal Reserve’s policy tightening would continue and perhaps ramp up. “We continue to believe markets underappreciate just how entrenched US inflation has become and the magnitude of response that will likely be required from the Fed to dislodge it,” advise economists at Nomura in a report to clients.

Fed funds futures are now pricing in a non-trivial possibility – an implied 38% probability as we write this morning — that the central bank will lift its target rate by 100-basis-points at the Sep. 21 FOMC meeting.

Former Treasury Sec. Larry Summers tweeted on Tuesday: “It has seemed self evident to me for some time now that a 75 basis points move in September is appropriate. And, if I had to choose between 100 basis points in September and 50 basis points, I would choose a 100 basis points move to reinforce credibility.”

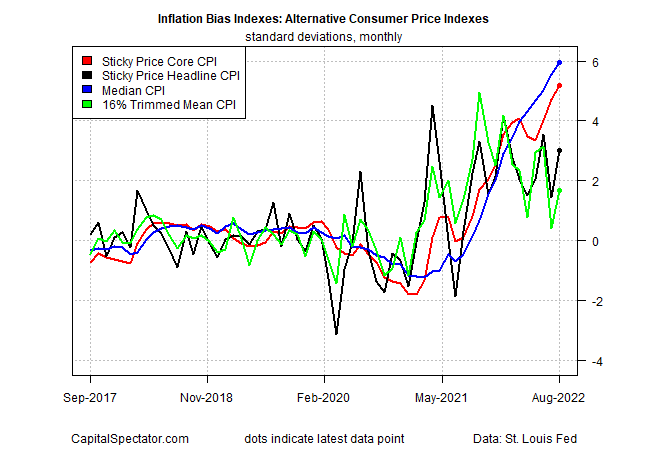

It’s not obvious that Summers is wrong when we look at CPI data via CapitalSpectator.com’s Inflation Bias Indexes. The methodology takes a standard inflation index, calculates the one-year change and then computes the monthly difference and transforms the results into standard deviations around the mean. This measure offers a way to develop some quantitative insight for deciding which way the inflationary wind is blowing.

On that basis, the recent decline in the inflation bias has stalled.

An alternative (and arguably more robust) set of consumer inflation measures, calculated by regional Fed banks, continue to paint a worrisome outlook, based on reviewing the data through CapitalSpectator.com’s inflation bias methodology noted above. Two of these indexes point to rising inflation pressure in August while two other benchmarks reflect persistent inflation pressures holding at elevated levels.

Overall, the numbers aren’t encouraging. High inflation is looking more entrenched, which in turn will likely spur the Federal Reserve to raise rates further for longer, and perhaps in bigger-than-recently expected increments. In turn, that lifts the odds that the economic growth will suffer, perhaps triggering a recession in the near term.

All of which reaffirms yesterday’s analysis that “Q4 is shaping up to be the acid test for the US economy’s resilience, or lack thereof.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report