The latest inflation data is sticky, but the markets have only delayed rather than canceled expectations for that the Federal Reserve will start trimming interest rates in the near future. Some analysts are pushing back on the idea, including forecasts in some quarters that the Fed may leave rates higher for longer. But judging by implied market estimates for changes in monetary policy, the central bank is still on track to cut in the near term.

The first cut is expected for the June 12 FOMC meeting, according to Fed funds futures, which are currently pricing in a roughly 77% probability for easing on that date, based on CME data this morning. By contrast, the futures market anticipates that no changes in the target rate are likely at the March 20 and May 1 meetings.

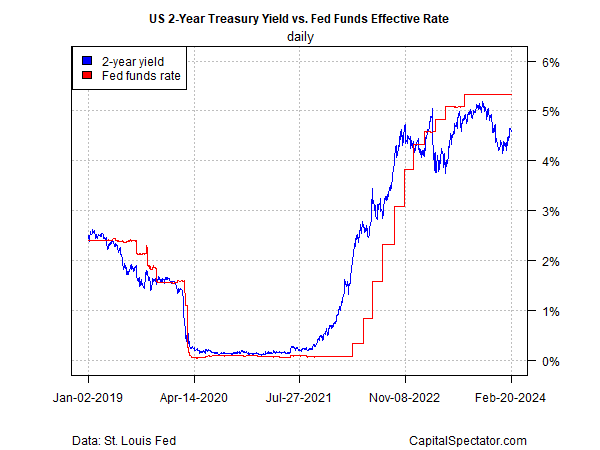

The Treasury market continues to price in rate cuts as well, based on the policy-sensitive 2-year yield, which is considered the most-sensitive spot on the yield curve for anticipating near-term policy. The 2-year yield was 4.59% yesterday (Feb. 20), substantially below the Fed’s current 5.25%-to-5.50% target rate (or roughly 5.33% at the median).

The implication: the Treasury market expects rate cuts in the near term. Of course, the market has been expecting that for more than a year, based on the 2-year yield, and the implied forecast has yet to play out as anticipated.

Reviewing a simple model that compares the Fed funds rate to inflation and unemployment suggests that policy is tight and so rate cuts are reasonable at this point.

Several monetary policy rules calculated by the Cleveland Fed paint a similar picture. The basic version of the so-called Taylor rule, for instance, suggests the current Fed funds rate should be substantially lower.

Nonetheless, there’s room debate. Start with the Cleveland Fed estimates: one model (First difference rule) suggests rates should go higher still.

Former Treasury Secretary Larry Summers says there’s a 15% chance that the Federal Reserve will continue to raise interest rates to tame inflation, which has slowed recently but gradually so, raising concerns that disinflation has stalled. “There’s a meaningful chance — maybe it’s 15% — that the next move is going to be upwards in rates, not downwards,” he told Bloomberg Television on Friday. “The Fed is going to have to be very careful.”

Atlanta Fed President Raphael Bostic, a current voting member on the Fed, on Friday said “we’ve seen a lot of progress in terms of inflation,” but the trend will be a “little bumpy” over the course of 2024. For now, he still expects rates cuts in the “summer time” he told CNBC and currently sees two cuts for 2024, which is fewer than implied by the full-calendar year outlook via Fed funds futures.

The next major reality check on expectations via data releases arrives next week (Feb. 29) with the January release of PCE Price Index data.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno