Cash led the performance race in August for the major asset classes, based on a set of proxy ETFs. In fact, most markets posted losses last month. The handful of winners, in addition to cash: a broad measure of commodities and US junk bonds.

The iShares Short Treasury Bond ETF (SHV), a cash proxy based on short-term government bonds with maturities of 1-year or less, rose 0.5% in August. The gain edged out a virtually identical increase for iShares S&P GSCI Commodity-Indexed Trust (GSG). A close third-place performer: SPDR Bloomberg High Yield Bond ETF (JNK), which posted a 0.3% advance last month.

The rest of the major asset classes ended the month in the red. The deepest decline in August: stocks in emerging markets (VWO), which tumbled a hefty 5.9%, marking the fund’s deepest monthly setback since February.

US stocks (VTI) also lost ground last month, albeit by a comparatively middling 1.9% decline.

Year to date, most of the major asset classes are still posting gains, led by a sizzling return for US shares (VTI), which are up 18.1% so far in 2023.

The downside outliers for the year so far: government bonds in developed markets ex-US (BWX) and foreign real estate (VNQI).

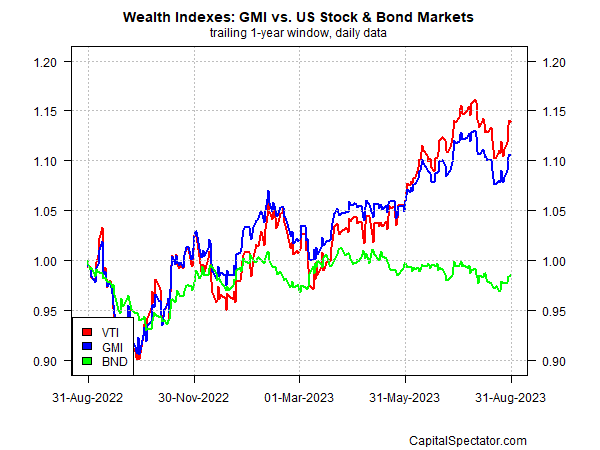

The Global Market Index (GMI) lost ground in August, dropping 2.3%, the first month decline since May. This unmanaged benchmark (maintained by CapitalSpectator.com) holds all the major asset classes (except cash) in market-value weights and represents a competitive benchmark for multi-asset-class portfolios. Despite the latest drop, GMI is currently posting a solid 10.5% year to date gain – ahead of all its component markets except for US shares (VTI).

GMI’s performance over the past year has echoed the gain for US stocks (VTI). US bonds (BND), by comparison, continue to post a modest loss for the rolling one-year period.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno