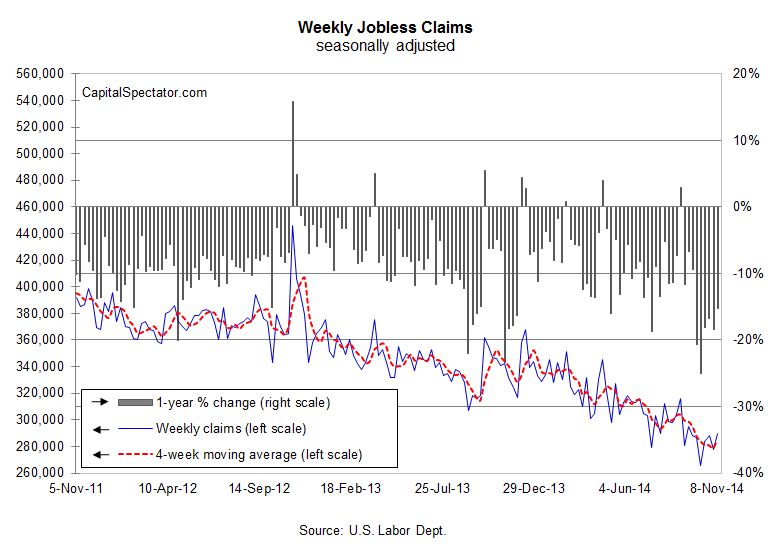

New filings for unemployment benefits rose more than expected last week, according to this morning’s update from the Labor Department. Jobless claims jumped 12,000 to a seasonally adjusted 290,000 for the week through Nov. 8—the highest since late-September. The latest numbers look a bit worrisome, but reviewing today’s figures in historical context suggests that a positive tailwind is still blowing for the US labor market.

Although the latest rise reflects a seven-week high, the increase remains comfortably within the downside channel that’s prevailed for much of 2014. Weekly claims numbers are quite volatile and so it’s essential to monitor this valuable leading indicator by way of its longer-term trend, including the four-week average and the more reliable year-over-year percentage change. On both counts, a bullish bias remains conspicuous.

Indeed, the seasonally adjusted four-week average for claims, although up modestly last week to 285,000, remains just above a 14-year low (279,000) that was set during the week through Nov. 1. Meantime, new claims continued to drop at a double-digit pace last week, falling 15.2% for the week through Nov. 8 vs. the year-earlier level. That’s still a relatively steep decline rate in terms of recent history and it signals ongoing growth for the US economy and job creation.

“The labor market is doing quite well,” Tom Simons, a Jefferies economist, tells Bloomberg. “It’s definitely beneficial for households. Better labor-market data and low gas prices should make for a good holiday season.”

Some analysts are worried that Europe’s economic stagnation and other troubles around the world threaten to derail the economic recovery in the US. Anything’s possible, but for the moment the US data look encouraging via jobless claims and a broad set of indicators. If growth is in fact slowing beyond US borders, as it seems to be, that’s certainly a risk factor. But for now it’s a risk factor that falls short of the critical level in terms of the immediate outlook for the US.

Will that change? No one knows, but if and when the macro climate for the US deteriorates in a meaningful degree, you’ll read about it here.

Meantime, the next stress test for the economic profile is tomorrow’s monthly retail sales report. The crowd’s expecting a modest revival for spending in the October figures, which would certainly be welcome after the previous month’s slide. For good or ill, tomorrow’s data will set the tone for the holiday shopping season that will kick off later this month with the arrival of Black Friday (Nov. 28).

Pingback: Thursday links: slow and boring | Abnormal Returns