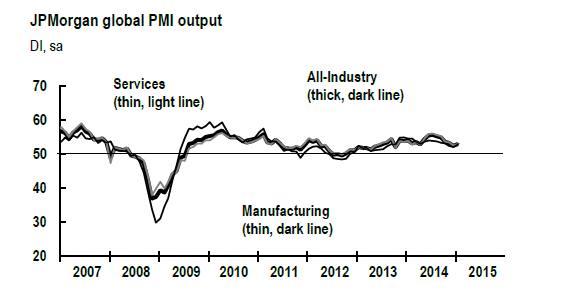

Growth picked up a bit at the start of the new year for the global economy, according to business survey data for January. The JPMorgan Global All-Industry Output Index ticked higher last month, rising to 52.8 from December’s 14-month low of 52.4. (A reading above the neutral 50.0 mark indicates expanding economic activity.) Yes, it’s a mild advance and it hardly marks a sharp reversal from the slowdown that’s been unfolding lately. But the worst fears from some corners of the economic forecasting realm look prematurely dark at the moment.

“The start of 2015 saw the Global PMI Output Index at last edge higher, halting the slowdown in growth signaled by the surveys in the latter half of last year,” JP Morgan’s David Hensley said in yesterday’s release. “Both manufacturers and service providers saw mildly stronger output expansions, keeping the global economy on a steady, yet moderate, growth path. Job creation also continued in January, which should aid in sustaining the upturn as well.”

The news may surprise some analysts, particularly those who’ve been predicting a global recession. Anything’s possible in the months ahead, of course, but global economic activity appears to be in no imminent danger of slipping into the business cycle ditch.

To be sure, there are still plenty of risks bubbling, including a softer run of growth for China that deserves close monitoring in the weeks ahead. But there have been some upside surprises, too, including a bit of growth for the perennially beleaguered Eurozone economy. The latest example: yesterday’s unexpected 0.3% rise in retail sales in December for the countries that share the euro—the fastest annualized gain in nearly eight years. It may not be sustainable, but suddenly the view that deflation is weighing on the real economy has a bit less traction in terms of the hard data.

Upbeat numbers from Europe are hardly limited to the latest consumer spending report. Other recent examples of growth from around the Eurozone include:

● Spain’s economy grew 0.7% in 2014’s fourth quarter and 1.4 percent last year, according to the National Statistics Office and official estimates for the year ahead anticipate a moderately faster expansion rate.

● German factory orders rebounded sharply in December after November’s slump, rising the most in six months. The news follows several months of improving sentiment in the investment and business communities via the ZEW and Ifo surveys.

● Markit’s composite business survey data for the Eurozone improved in January, reflecting mild growth at a six-month high.

● Now-Casting.com’s recent estimates of Eurozone GDP have ticked up lately, anticipating sluggish growth, which represents an improvement from previous forecasts of a slight contraction.

One could easily cite Europe’s many problems to paint a darker outlook, including the fresh uncertainty related to Greece’s new-found politically driven push to renegotiate the harsh austerity rules that are pinching its economy. By some accounts, the road ahead will bring a new round of turbulence that could lead to a Grexit—a traumatic event, if it occurs, that may unleash an economic tsunami in Europe. That’s still a low-probability risk, but the stagnation in Italy and France’s sluggish growth aren’t so easily dismissed.

Based on the numbers in hand at the moment, however, it seems that the global economy is still growing, albeit moderately so. The foundation continues to be a solid expansion in the US, even if the recent forecasts of accelerating growth for the world’s biggest economy look overly optimistic at the moment.

Meanwhile, recent data for the UK and Japan imply that growth still has the upper hand. Sharply lower energy costs in the wake of crude oil’s slide in recent months will provide an extra tailwind for keeping the expansion alive.

Perhaps the critical variable in the months ahead will be China, which is struggling with a slowing economy. The latest efforts by the country’s central bank to juice growth by cutting reserve requirements is a sign that the macro trend in China has a downside bias these days.

No one should underestimate the potential for trouble, but at the same time it’s fair to say that forward momentum remains the dominant theme for the global economy. The bottom line: doubting the world’s capacity for growth overall in the near term still looks like a bet with long odds.