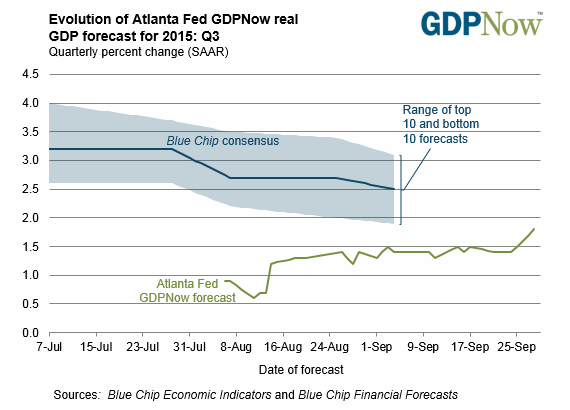

Today’s encouraging update on US personal income and spending for August raised the Atlanta Fed’s third-quarter GDP nowcast to 1.8% from 1.4% (seasonally adjusted annual rate). The revised GDP projection for the current quarter is still a sluggish pace and well below Q2’s strong 3.9% increase. But at least the revisions are moving in a positive direction. In fact, today’s update of the widely followed GDPNow model offers the highest growth rate since the Fed bank began publishing Q3 estimates in early August. That’s not saying much since the initial estimate was a tepid 0.9%. Nonetheless, in the current environment of bearish expectations, the sight of even minor upgrades for macro expectations is noteworthy.

The upwardly revised Q3 GDP projection is hardly a game changer. There’s still a strong case for expecting slower growth for the US as we head into the final months of the year. But today’s modestly brighter outlook suggests that the worst fears may be overbaked.

Cautious optimism for the near-term is also the message in last week’s September update of Markit’s Composite PMI Output Index for the US. This benchmark, which combines sentiment data from the services and manufacturing sectors, fell slightly to 55.3 in this month’s flash reading from 55.7 in August. But that’s still well above the neutral 50 mark and it offers support for expecting moderate growth to prevail for the foreseeable future.

Global events in the weeks ahead could deliver an alternative narrative, for any numbers of reasons–including worrisome numbers for China’s current bout of decelerating growth. But based on the figures for the US, it’s getting harder to argue that the world’s biggest economy is on course for a fatal stumble in September.