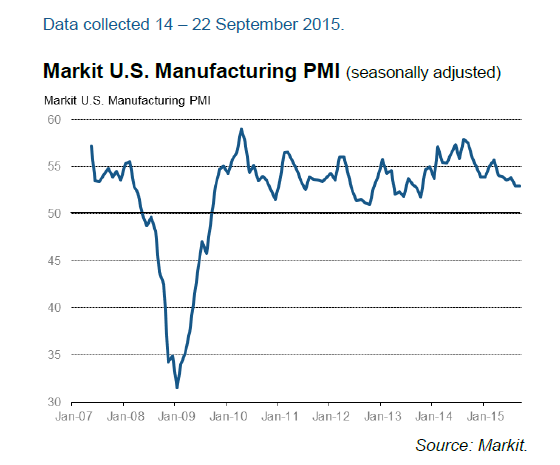

US manufacturing activity is surprisingly firm in September, according to the initial estimate of Markit’s purchasing managers’ index (PMI) for this corner of the economy. I say “surprisingly firm” because three previously released regional indexes for manufacturing in September (via Fed banks) are unusually weak, as I discussed yesterday. But the national trend for manufacturing looks comparatively resilient. Growth is still moderate, bordering on sluggish for manufacturers. But if you’re looking for a dark signal for the US business cycle, today’s PMI update doesn’t offer much red meat.

That said, manufacturing output “remains at the lowest level since October 2013,” Markit advised in today’s press release. The good news is that the flash reading of this month’s headline PMI is 53.0, unchanged from August. A number above the neutral 50 mark indicates growth, which means that today’s update reflects a modest pace of expansion for this cyclically sensitive sector. The fact that the PMI is steady and in positive territory suggests that the US macro trend isn’t giving way to the darkness that appears to be descending elsewhere in the world, particularly in some emerging markets, including China. Indeed, China’s manufacturing PMI for September (also released today) slipped deeper into negative territory this month: 47.0 vs. 47.3 in August.

But if there’s no clear and present danger signal here for the US, it’s not exactly encouraging news either. “The survey is indicating the weakest manufacturing growth for almost two years, meaning the sector will have acted as a drag on the economy in the third quarter,” says Chris Williamson, chief economist at Markit.

No wonder that expectations for US third-quarter GDP growth are subdued these days. As outlined yesterday, most analysts are looking for a relatively hefty round of deceleration in the rate of growth for Q3 GDP vs. Q2. The Wall Street Journal’s average Q3 GDP estimate, based on this month’s survey of economists, is 2.4%–down sharply from the 3.7% rise in the second quarter (seasonally adjusted annual rate).

Today’s PMI update doesn’t offer much incentive for raising growth expectations, although the Markit release doesn’t support folks who see a US recession around the next bend either. The PMI report does, however, offer another data point for expecting that the US economy will muddle through with a modest expansion.

Pingback: US Manufacturing Firm for September