How’s that second-quarter rebound holding up? Well, it’s shaky. The economic reports in the weeks ahead could tell us otherwise, but the numbers published so far for May offer a mixed bag of results for the US economy.

Let’s start with the good news. The outlook is certainly positive from the vantage of jobless claims. But using other numbers to guesstimate this month’s macro pace temper any optimism that May will deliver solid improvement over April’s sluggish profile. It’s still early and so the tepid results overall are subject to change. But for now, the figures in hand suggest that second-quarter growth will be modest.

On the plus side, jobless claims continue to trend lower and two of three regional Fed indexes that track business sentiment are moderately positive. The initial estimate of Markit’s business survey data for manufacturing, however, reveals that growth decelerated in May to the slowest pace in 16 months. Meantime, consumer sentiment slumped in May. Perhaps, then, it’s no surprise that the Atlanta Fed’s May 19 estimate for second-quarter GDP growth is stuck at a soft 0.7%–only slightly higher vs. Q1’s stall-speed increase of just 0.2%.

Here’s a closer look at the key indicators available to date for the May economic profile:

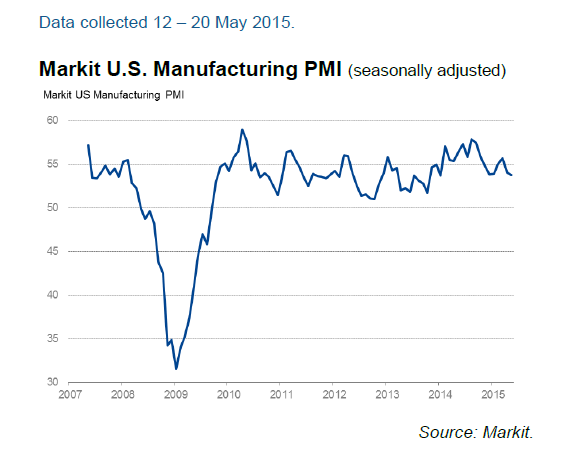

Markit Flash US Manufacturing PMI

Manufacturing activity remains moderately positive in May, but the flash estimate of Markit’s purchasing managers’ index for this corner of the US economy dipped to the slowest pace of growth in 16 months. “Manufacturers reported their weakest growth since the start of 2014 in May, with the survey results adding to fears that the strong dollar is weighing on the US economy and hitting corporate earnings,” said Chris Williamson, chief economist at Markit Economics.

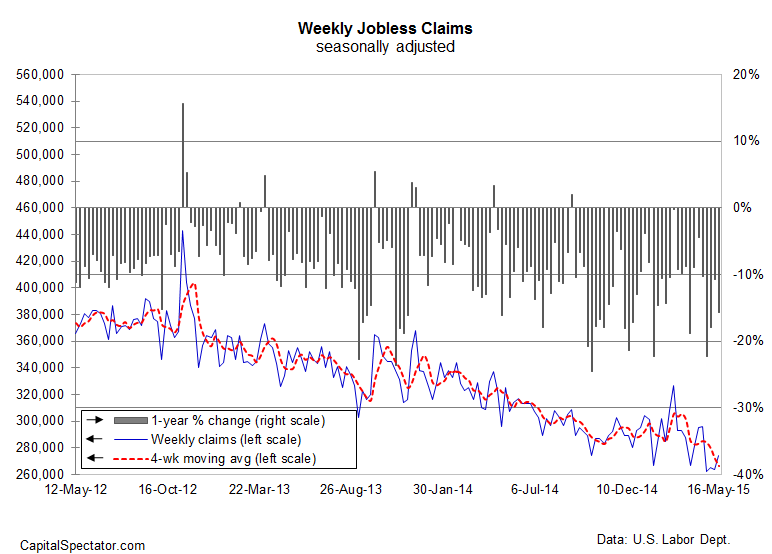

Jobless Claims

New filings for unemployment benefits continue to trend lower, dispensing a bullish signal for the labor market and, by extension, the US economy. Although jobless claims increased last week, filings remain close to a 15-year low. Meanwhile, claims fell by nearly 16% last week vs. the year-earlier level, signaling that payrolls are on track for a solid rate of growth in the near-term future. For the moment, jobless claims are the main source for anticipating a robust pace of US economic growth.

Atlanta Fed’s Q2 GDP Nowcast

The Fed bank’s May 19 estimate of US economic growth for this year’s second second is a weak 0.7%. The current estimate is up slightly from GDP’s fractional 0.2% rise in Q1.

Regional Fed Indexes

Two of three business-activity benchmarks via regional Fed banks are in positive territory this month, albeit mildly so. Notably, the New York Fed’s index moved above zero this month after a mild retreat below zero in April. Meanwhile, the Kansas City Fed Index fell deeper into the red in May. The median change for the May data published to date, however, posted its first rise since February.

Consumer Sentiment

Consumer sentiment in May dropped to its lowest level in seven months in the preliminary May estimate of Thomson Reuters/University of Michigan’s index. “Confidence fell in early May as consumers became increasingly convinced that there would be no quick and robust rebound following the dismal (first) quarter” said Richard Curtin, chief economist at Michigan’s Survey of Consumers. Sentiment data from other sources also point to a deterioration in the mood in the consumer sector. Bloomberg’s weekly Consumer Comfort Index dipped to a new year-to-date low for the period through May 17. Meanwhile, Gallup’s Economic Confidence Index—a measure of Americans’ views of current economic conditions—fell slightly for the weekly reading through May 17, a level that’s close to the lowest level so far this year.

Pingback: 05/22/15 - Friday Interest-ing Reads -Compound Interest Rocks