Last week’s surprisingly strong gain in November payrolls may be a sign that the US economy is improving, but you wouldn’t know it by looking at the Treasury market. Or would you? Actually, much depends on which portion of the yield curve you’re gazing at. The 2-year yield has popped higher since Friday’s bullish payrolls data, which is what you’d expect for this maturity — typically the most sensitive slice of the curve when it comes to rate expectations. But the analysis is complicated by tumbling inflation expectations.

Economist Tim Duy advises “that there is a tendency to underestimate the potential for a more hawkish Fed,” explaining that “policymakers have been falling in line with the idea of a mid-2015 rate hike, somewhat earlier than market expectations.”

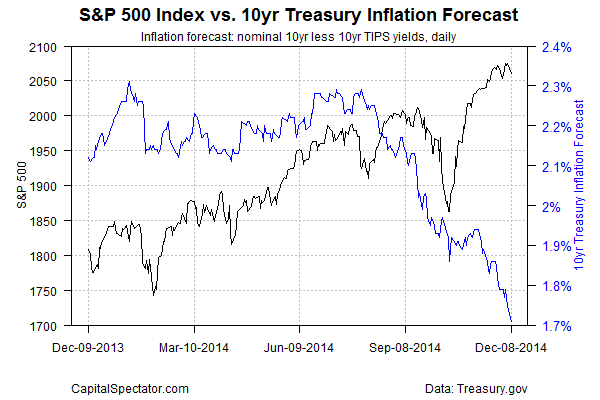

That’s a reasonable view based on the macro fundamentals of late, especially in the wake of the latest jobs report. But the world of Treasuries isn’t of one mind on such matters, or so one can argue based on the market’s implied inflation forecast via the yield spread on the nominal 10-year Note less its inflation-indexed counterpart. Indeed, this spread slumped to 1.71% yesterday (Dec. 8), the lowest since Sep. 2011—a time, it’s worth remembering, when macro projections were considerably less enthusiastic vs. the current outlook.

The view looks quite a bit different by way of the 2-year yield, which has climbed sharply in the last several days relative to its recent range.

By some accounts, we’re in a conundrum. A stronger economy should be raising inflation expectations and yields, across the maturity spectrum. That, at least, is what history tells us, albeit a history since the 1970s. But a longer view offers a different perspective, and arguably a more reliable guide for what’s coming, namely, an extended run of low inflation. “Over time, what drives the bond yield is the inflationary expectations,” Lacy Hunt, the chief economist at Hoisington Investment Management, told Bloomberg last week. “If you wring all the inflationary expectations out, you are going down to 2 percent on the long bond over the next several years. That is the path that we are on.” The yield on the long bond (30-year Treasury), by the way, was 2.90% yesterday, Dec. 8—close to the lowest level in over a year.

Low inflation in recent years has been a sign of trouble, thanks to the lingering effects of the 2008 financial crisis and the Great Recession. But yesterday’s problems may no longer apply. If the US is truly on a path of moderate growth or better, low and stable inflation is a good thing. There are caveats, of course. Low-flation with weak growth or worse spells trouble, which is the diagnosis that currently applies to Europe and Japan. The US, by contrast, seems to have the best of both worlds these days—low inflation and moderate growth if not something better.

As an added bonus, US Treasury yields are partly sensitive to global macro forces, which have a distinctive disinflation/deflationary bias of late, particularly on an ex-US basis. But therein lies opportunity. To the extent that the US can maintain a respectable expansion, the global demand for bonds will go a long way in keeping borrowing costs low. Even better, energy costs are falling and may stay low for an extended period.

The bottom line: An economy that’s growing at a decent rate can do quite well in a world of low inflation. The question is whether the US can remain an island of resilience when economies elsewhere are stumbling? So far, the numbers suggest this divergence can endure. “The market is struggling with the global growth story and the US story,” observes Gennadiy Goldberg, an interest rate strategist at TD Securities. For now, it’s a struggle that with a fair amount of upside for the US economy.

Pingback: Low Inflation and Moderate Growth Can Be a Good Thing