The answer depends on how you define “safe.” That’s a long conversation because every investor has a unique risk tolerance, time horizon and investment objective. What appears “safe” to you could frighten the hell out of your neighbor. Despite the caveats, we can at least start to think about how the odds stack up when the market takes a dive by crunching some numbers.

Perhaps the first observation is that that taking advantage of sharply lower prices is usually a good choice. Because prices move inversely to expected return, buying stocks after, say, a 20% haircut equates with investing at a time when expected return has jumped by a comparable degree. Of course, there’s a time factor to consider. Realizing the higher expected return will (probably) take years.

A reasonable way to smooth out the noise is dollar-cost-averaging. Regular investments into the market mechanically buys more (less) when prices fall (rise), relieving you of the task of estimating timely moments for investing.

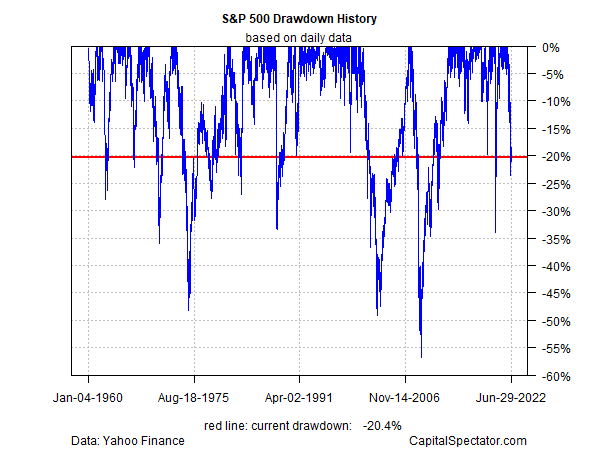

If you’re inclined to be clever, a first step might be looking at how drawdown informs expectations. For example, the S&P 500 Index is currently nursing a 20% drawdown (as of June 29). Declines of that magnitude or deeper are commonly labeled as “bear markets.” More importantly, history suggests that when the S&P 500 falls 20% from its previous peak, there’s usually more pain to come before the market finds a bottom. On that basis, the odds don’t appear to be in our favor at the moment that the worst has passed, or so history implies.

Another way to gauge how the current correction compares with its predecessors is by comparing (in Z-scores) how the market’s current 50-day average less its 200-day average stacks up. Let’s call this the Peak Risk Index. By this measure, the slide is about as deep as it gets via the historical record since 1960. Does that mean that the worst has passed? Maybe, but this alone is no guarantee that we’re at a bottom. What it does tell us is that the magnitude of the decline, so far, is quite steep in relative terms. Nonetheless, there’s no assurance that a market that appears to have fallen off a cliff can’t stay depressed, or go lower still. That said, if your risk tolerance is relatively high you might be inclined to interpret the data as a signal for betting on a bounce.

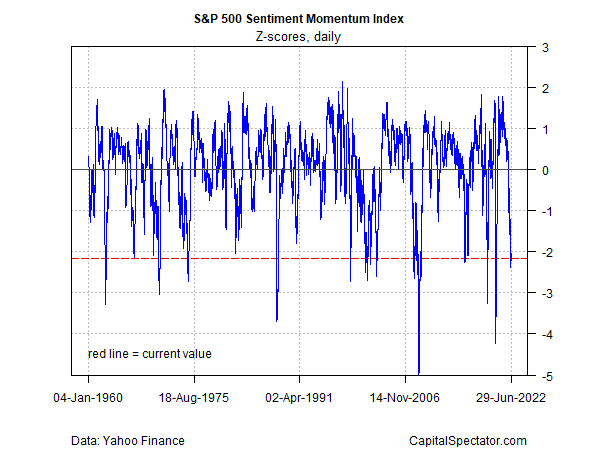

Finally, let’s look at a somewhat more-nuanced version of the Peak Risk Index in search of a more robust reading of how the market correction compares. In this case we’re looking at a 7-factor analysis of the S&P 500’s degree of directional bias – the Sentiment Momentum Index (SMI). For design details, see here.

The main takeaway: the market’s dive, although relatively deep, has yet to reach the maximum depths previously recorded. That’s a basis for remaining cautious for thinking that the correction has run its course.

If you’re highly risk averse, you might look at SMI and wait for the index to bounce to a relatively high level. In a follow-up post, I’ll look at the history such bounces for deciding when it’s truly “safe” to go fishing again. The obvious drawback: the “safer” the outlook, the more you leave on the table in terms capturing relatively higher expected returns. Then again, waiting for a bounce minimizes the risk that you got in too early. Therein lies the art of investing: balancing risk and return. There’s no right (or wrong) answers, but there are countless variations in risk tolerance, which is to say countless ways to interpret the numbers.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report