Earlier this year a number of economic analysts were convinced that a US recession was imminent. So far, however, the economy has continued to expand, albeit at a slowing pace as the year unfolded. The breathless warnings have, once again, come to naught — par for the course in recent years. The culprit, as usual: misguided business-cycle analytics.

That doesn’t mean that an all-clear signal has arrived as the year winds to a close. But reviewing the past warnings, and what most analysts got wrong, can tell us a lot about how to model recession risk to minimize the noise and maximize the signal.

The first step is to understand what not to do. Perhaps the biggest mistake is to focus on a lone indicator. For example, an economist back in January predicted that 2019 was likely to suffer the start of a new downturn. The catalyst? “We’ve got more than 80 percent chance of recession just based on the fact the Fed is tightening policy,” he warned on CNBC.

Some readers will counter that focusing on the yield curve has proven to be a reliable gauge of future recession risk. And on that front, another dismal scientist recently said this indicator was all-in on predicting that a new contraction was more or less fate. After the 10-month less 3-month spread for Treasury yields inverted for a full quarter through June 30, 2019, an official recession forecast was triggered, or so this line of reasoning advised.

Considering that this indicator has preceded every previous recession since the 1960s implies that this is an infallible metric. Perhaps it is, but no one can know that with confidence as it applies to the future. Meanwhile, using the New York Fed’s estimate of recession risk based on the Treasury spread (for data through November) shows that this measure of recession risk has recently peaked and is now falling. The implication: a recession must start soon to avoid a false signal for this indicator.

The median for a set recent nowcasts of fourth-quarter GDP, however, suggests that the economy will continue to muddle onward. The slow-growth trend in Q3 looks set to continue in the final quarter of this year, but that’s probably strong enough to keep the recession demon at bay.

Relying on one indicator, even one with a solid history, is still asking for trouble. Why? The short answer: things change and so it’s not always clear that the conditions that led to clear signals in the past will continue in the future. For instance, the Fed may be more proactive these days in trying to extend the current expansion. If so, the reliability of the yield curve could suffer as a recession warning.

More generally, predicting recessions is a sketchy affair. Prakash Loungani, an IMF economist who’s studied economic forecasting records, observes that “very, very few recessions have been predicted nine months or a year in advance.”

To the extent that you’re looking forward, the lesson is that a short time horizon is preferred. The 1-2 months forecasting window that are used in The Capital Spectator’s monthly business-cycle analyses, for instance, have proven to be relatively reliable estimates of the trend. Here, for example, is last month’s update (see chart at bottom of post). Each monthly column has links to previous updates, allowing readers to judge for themselves how the estimates stack up through time.

Note, however, that the reliability of The Capital Spectator’s business cycle analysis is predicated on a model that draws on a broad, diversified set of economic and financial indicators and using a robust methodology to forecast the aggregated signal one-to-two months in advance. Sticking to short forecasts by itself doesn’t help much if you’re doing so with a flawed model.

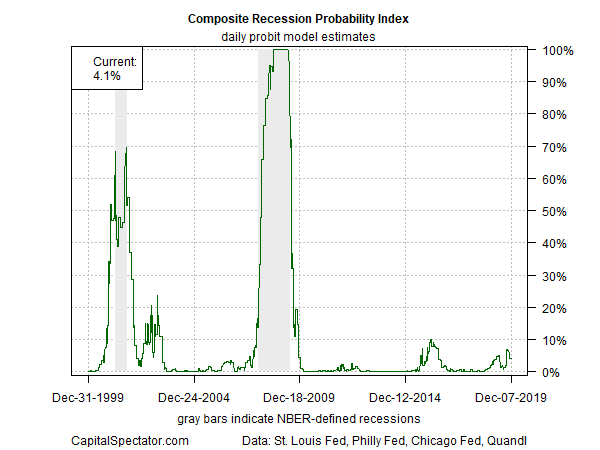

Despite the encouraging track record of The Capital Spectator’s proprietary business cycle indexes, relying on these benchmarks still doesn’t suffice. To further strengthen real-time recession signals it’s valuable to aggregate these indexes with other business-cycle benchmarks and run the data through a probit model to estimate real-time estimates of the probability that an NBER-defined contraction has started.

That’s exactly the goal of the Composite Recession Probability Index (CRPI), which combines five business cycle indexes, including the Philly Fed’s ADS Index and the 3-month average of the Chicago Fed National Activity Index. Not surprisingly, CRPI is robust measure of real-time recession risk – a signal that hasn’t been confused by the recent economic noise. For example, here’s CRPI’s print at the end of last week, as published in the Dec. 9 issue of The US Business Cycle Risk Report.

Searching for the sweet spot in real-time recession analysis is tricky because it requires balancing the dual goals of timeliness and reliability. Elevating one usually comes at the expense of degrading the other. Pick your poison? Maybe not. History suggests that CRPI excels in balancing these twin goals. For example, CRPI reflected low recession risk back in April – when many analysts were warning that a new recession was near.

The main hazard for many investors trying to assess the state of macro risk: succumbing to the illusion that there’s an easy way to evaluate recession probability. Casually looking at a handful of indicators may sound like a good idea, but quite often it only leads to a muddled outlook.

Fortunately, a relatively clear, reliable and timely signal is available through a disciplined approach that measures a diversified set of metrics that capture the full sweep of the US economy. The bad news for the casual observer: the usual suspects don’t offer this data.

Where does that leave us today? Recession risk is still low and an NBER-defined recession isn’t likely to begin in the immediate future. But this analysis has a short shelf life – 24 hours, which is why crunching the data anew every day, with a robust model, is the only defense against an uncertain future and misguided business-cycle analytics.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Predicting Recessions Is a Sketchy Affair. - TradingGods.net