Tail Risk Management for Multi-Asset Multi-Factor Strategies

David Chambers (University of Cambridge), et al.

January 8, 2019

Multi-asset multi-factor portfolio allocation is typically centred around a risk-based allocation paradigm, often striving for maintaining equal volatility risk budgets. Given that the common factor ingredients can be highly skewed, we specifically incorporate the notion of tail risk management into the construction of multi-asset multi-factor portfolios. Indeed, we find that the minimum CVaR concentration approach of Boudt, Carl and Peterson (2013) effectively mitigates the dangers of tail risk concentrations. Yet, diversifying across multiple assets and style factors can be in and of itself a good means of tail risk management, irrespective of the risk-based allocation technique employed.

Continue reading

Daily Archives: May 10, 2019

Macro Briefing: 10 May 2019

Trump raises tariffs on China, which vows to respond: CNBC

US-China trade talks to resume today: CNN

Estimates of economic costs to higher tariffs in US-China trade war: MW

US seizes N. Korean ship that violated international sanctions: AP

UK economic growth strengthened in first quarter: BBC

Jobless claims in US fell last week, near 50-year low: MW

US producer prices increased less than forecast in April: WSJ

US trade deficit increased slightly in March: MW

BlackRock strategist: yield curve losing predictive power: Bloomberg

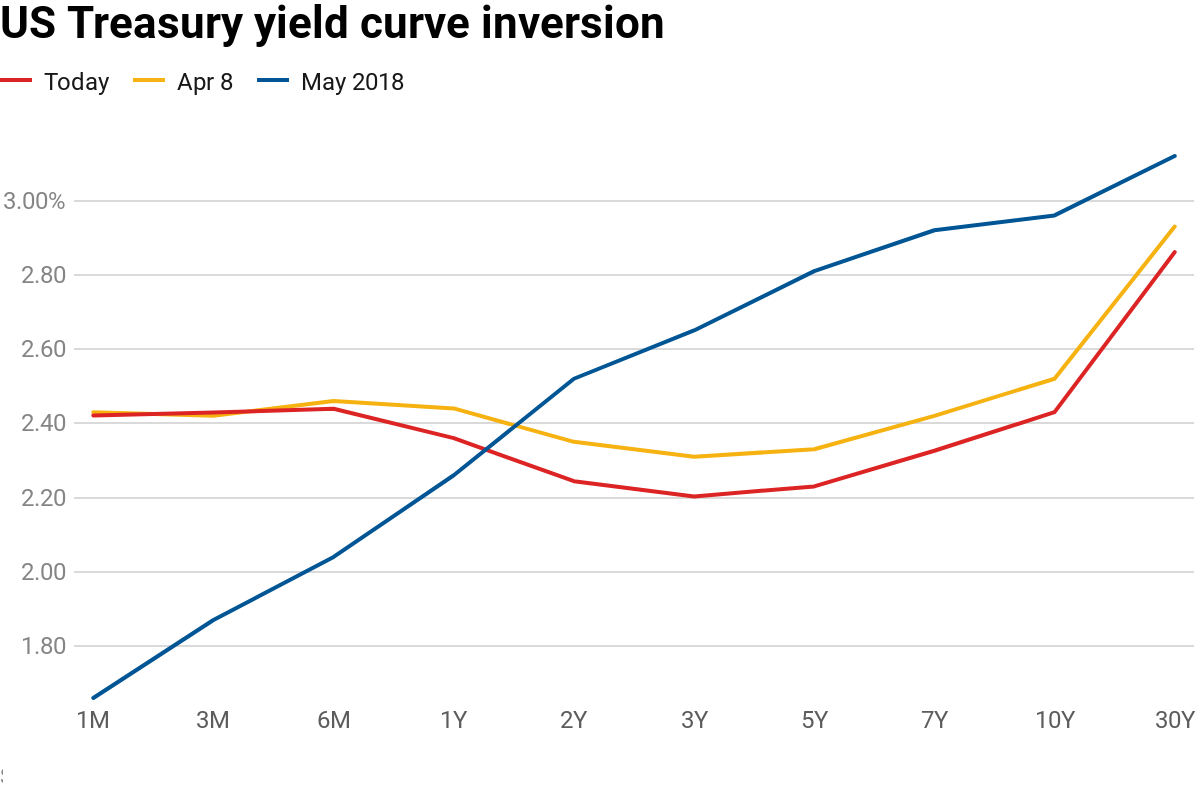

10yr-3mo yield curve goes negative, suggesting higher recession risk: CNBC