In the quest for clarity in portfolio analytics, Professor Bill Sharpe’s introduction of returns-based style analysis was a revelation. By applying statistical techniques to reverse engineer investment strategies using historical performance data, style analysis offers a powerful, practical tool for understanding the source of risk and return in portfolios. The same analytical framework can be used to replicate indexes with ETFs and other securities, providing an intriguing way to invest in strategies that may otherwise be unavailable.

Continue reading

Daily Archives: October 10, 2017

Macro Briefing: 10 October 2017

Raging wildfires destroy thousands of Northern California homes: USA Today

Richard Thaler wins Nobel for behavioral economics research: The Atlantic

EPA chief says wind and solar tax credits should be eliminated: The Hill

Turkey-US diplomatic crisis deepens: Bloomberg

Is Spain’s Catalonia crisis an investment opportunity? Bloomberg

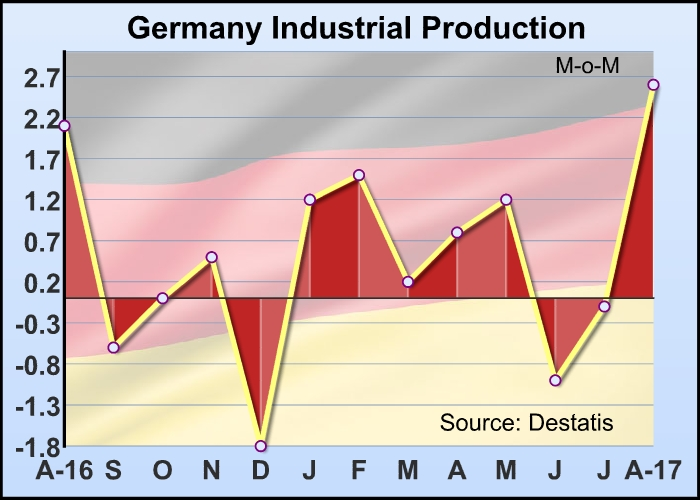

German industrial output in Aug posts the strongest rise in 6 years: RTT