Treasury yields continue to fall, making mincemeat of the idea that the Federal Reserve will continue to raise interest rates this year. Everything could change, of course, if the incoming economic data turns out to be stronger than expected. The main event for this week: January payrolls, starting with today’s preliminary estimate for the private sector via ADP’s data, followed by Friday’s official numbers from the US Labor Department. Meanwhile, Mr. Market has been slashing rates across the Treasury curve in the wake of revived worries about economic growth.

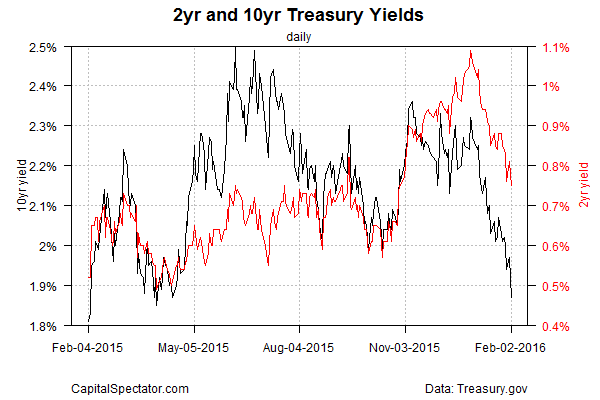

The 2-year yield—considered the most sensitive for rate expectations—has fallen sharply this year, decreasing to a three-month low of 0.75% yesterday (Feb. 2), based on daily data from Treasury.gov. The benchmark 10-year yield’s tumble is even more dramatic, sliding to 1.87%–the lowest level since last April.

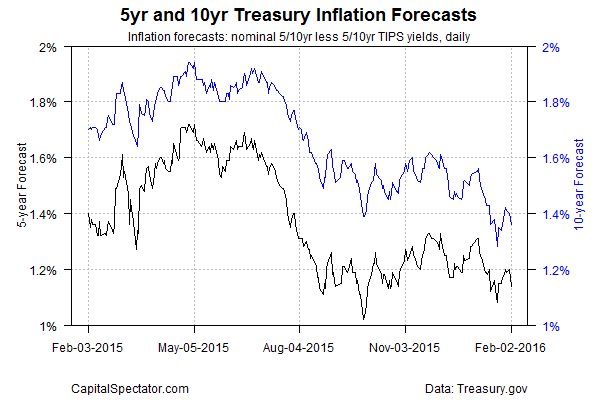

There’s a bit of good news in that the market’s five-year inflation expectations remain relatively stable, albeit at subdued levels vs. recent history. Future inflation implied by the yield spread for the nominal 5-year yield less its inflation-indexed counterpart is currently 1.14% as of Feb 2. That’s a middling rate in the context of the last several months, but for the moment it’s encouraging to see that it’s not collapsing. The 10-year inflation forecast, however, looks weaker in context with its recent range and so there’s still plenty of uncertainty about what happens next.

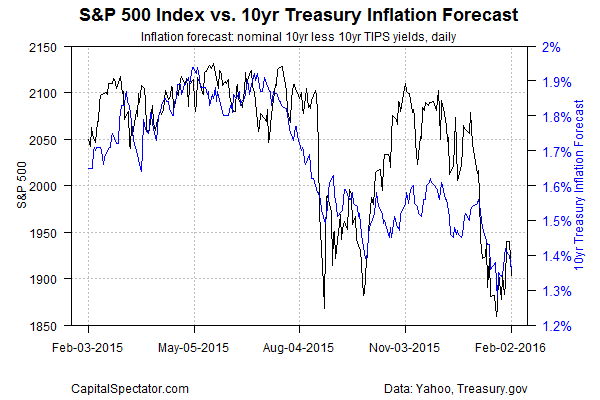

Note that the US stock market (S&P 500) and the implied 10-year inflation rate are again moving in lockstep, and for all the wrong reasons. The recent slide in equities has been accompanied by a drop in inflation expectations. The return of a tight correlation here is a sign that the crowd’s becoming increasingly anxious about disinflation/deflation risk. That’s a worrisome development, particularly if it continues and the outlook for inflation trends lower. Accordingly, this is a clue that the Fed should refocus efforts on raising expected inflation.

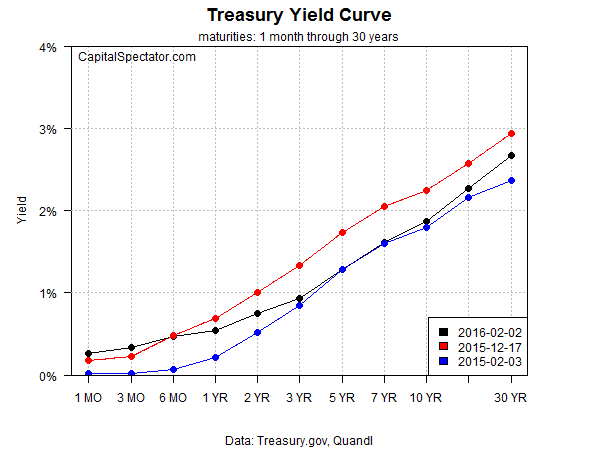

Meanwhile, the Treasury yield curve is still positively sloped, which suggests there’s still time for the Fed to act. Letting the curve invert, which is now looking like a possibility for the near-term future, would send a dark signal for the macro trend. But time may be running out. As you can see in the chart below, the curve has flattened a bit lately. Yields for maturities at 1-year and above as of yesterday (black line below) have slipped below levels of 30 trading days earlier (red line) by more than a trivial degree.

A reprieve may be near, however, if the upcoming numbers on payrolls deliver upbeat news. Economists think we’ll see a decent gain in today’s ADP Employment Report for January—ditto for Friday’s update from the Labor Department, based on the consensus forecast via Econoday.com. But note that in both cases the expectations call for substantially softer advances vs. the previous two updates. Analysts reckon that private-sector payrolls in January are on track to rise by 180,000 in Friday’s estimate from the government–a sharp deceleration from the strong gain of 275,000 in the previous month.

That’s not terrible, but in the current climate of diminished expectations it’s a news story that may push yields even lower. In that case, the recent estimates of low recession risk for the US (based on figures through December) may suffer in the next batch of revisions.

Pingback: Treasury Yields Continue to Fall

Pingback: 02/03/16 – Wednesday’s Interest-ing Reads | Compound Interest-ing!