The astonishing bull market (bubble?) in Bitcoin has drawn attention to the cryptocurrency from all corners. One of the questions that’s reasonating: Should Bitcoin be treated as an asset class, on par with stocks, bonds, real estate and commodities?

A Forbes article last year, citing a study by ARK Investment Management, offered “4 Reasons Why Bitcoin Represents A New Asset Class.” The firm, which Forbes labeled as the first public fund manager to invest in Bitcoin, argues that the low correlation is a key variable for the decision.

“If an investor who holds bonds and equities swapped a percentage of their prior holdings into bitcoin, because of bitcoin’s low correlation and superior absolute performance, they could have decreased the volatility of the portfolio while simultaneously increasing absolute returns,” opined Chris Burniske, an analyst at ARK and co-author of “Bitcoin: Ringing the Bell for a New Asset Class.” The low correlation, he asserts, “is the golden bullet of an asset class.”

Perhaps, but skeptics might wonder how much of Bitcoin’s allure as an alternative asset class is bound up its extraordinary rise of late. It’s doubled in just over the last three months. Longer term, the gain is even more impressive — off the charts, in fact. Valued at just a few pennies in mid-2010, it was trading yesterday around $2,800, according to Coindesk.com.

Whatever you think of Bitcoin (and its various competitors, such as Ethereum), there’s at least one fact that everyone can agree on: price changes for Bitcoin and its rivals are extraordinarily volatile. That’s good news if you’ve been long the currency of late, but upside volatility has a dark side. Bitcoin drawdowns in the past have been extreme to the point of making changes in the stock market look like a money market fund by comparison. Bitcoin, it’s fair to say, is not a marketplace for the feint of heart.

Nonetheless, some intrepid investors/speculators are considering Bitcoin and the like as a worthy addition to a conventional asset allocation plan. That’s a tempting argument while the returns of recent vintage are in the stratosphere. Let’s see how the argument holds up when/if Bitcoin crashes.

In the meantime, let’s model Satoshi Nakamoto’s brainchild relative to the usual suspects, if only as an academic exercise to see how Bitcoin (BC) stacks up. For some context, let’s begin with wealth indexes, using a start date of July 19, 2010, which is initial price in Coindesk.com’s BC time series. For context, wealth indexes for six ETFs are also included in the chart below.

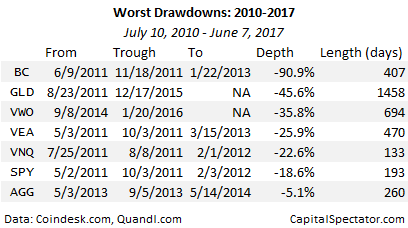

SPY: SPDR S&P 500

VNQ: Vanguard REIT

VEA: Vanguard FTSE Developed Markets

VWO: Vanguard FTSE Emerging Markets

AGG: iShares Core US Aggregate Bond

GLD: SPDR Gold

It’s clear that BC has been the top performer by an extremely wide margin. Even though the chart above shows performance results in log scale, the ETFs barely register against BC’s bull run over the past seven years.

BC’s road to riches, however, has been a white-knuckle ride in the extreme. Consider, for instance, daily return volatility. BC’s annualized standard deviation is an eye-popping 97% for 2010-2017 – a world above the US stock market’s roughly 15% via SPY. But the extreme vol has paid off, at least so far. BC’s annualized performance is off the charts at around 280% a year! SPY’s annualized return over the sample period is a relatively mild 15%, although that’s actually quite high by historical standards for equities.

But astronomical gains tend to be accompanied by the equivalent on the downside, and BC is no exception. The worst drawdown for the cryptocurrency since 2010 has been a punishing 91%. The US stock market’s biggest drawdown is tame by comparison at less than 19%.

From a diversification standpoint, BC’s returns show almost no correlation with other asset classes. Compared with US equities (SPY), for example, the correlation of daily returns vs. BC is close to zero for the past seven years. Similar numbers apply for foreign stocks, US bonds, real estate investment trusts, and gold. (Note: a correlation of 1.0 equates with perfect positive correlation; 0 indicates no correlation; and -1.0 reflects perfective negative correlation.)

But correlation alone shouldn’t dictate decisions on whether to add assets to a portfolio. Other key factors include expected return through time, and on that front BC is a bit of a mystery since estimating fair value is virtually impossible. The same can be said of gold, oil, and other assets that don’t generate cash flows or pay dividends, although most commodities have direct links to the real economy and so there’s a basis for a dedicated allocation in this corner.

Bitcoin, by comparison, is highly speculative. It’s also tiny market — total capitalization is less than $50 billion at the moment, according to Coindesk.com — a small fraction of, say, Apple’s market cap of $800 billion-plus. The relatively small marketplace suggests that BC could be manipulated by a few large players.

For most investors, BC is simply too hot to handle. Even for folks with a high tolerance for risk and a long time horizon it’s hard to rationalize putting more than a tiny percentage of serious money into BC, especially after it’s exploded to the upside over the past year.

But prepare to hear otherwise. As long as the Bitcoin gravy train rolls on, the arguments for buying will sound increasingly persuasive. But no matter how high BC flies, it’s destined to remain a high-risk asset that’s difficult if not impossible to value and prone to dramatic crashes out of the blue. For most folks, that’s a signal to steer clear.

Pingback: Breaking News And Best Of The Web - DollarCollapse.com

Pingback: Quantocracy's Daily Wrap for 06/11/2017 | Quantocracy

Pingback: Retail Banking Academy news roundup - 12/06/2017 - RBA Blog

Pingback: What we are reading on 6/13/2017 - UNDERVALUED STOCKS