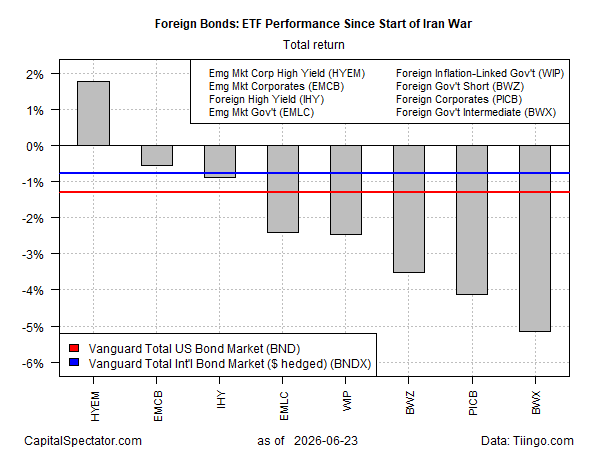

The Middle East conflict may have ended, but the damage lingers for foreign bonds from the perspective of US investors, based on a review of ETF performance from the start of the war on Feb. 28 through yesterday’s close (Jun. 23). The main headwinds: inflation worries and a rising US dollar.

Most segments of offshore bonds have lost ground since the war began, but one market stands out as a notable exception: high-yield fixed-income securities issued in emerging markets. The VanEck Emerging Markets High Yield Bond ETF (HYEM) has gained 1.8% since Feb. 28. That modest advance contrasts with broad losses across the rest of the field, led by a 5.2% decline in developed-market government bonds with intermediate maturities (BWX). Even the US investment‑grade benchmark (BND) has slipped, shedding 1.3% over the same period.

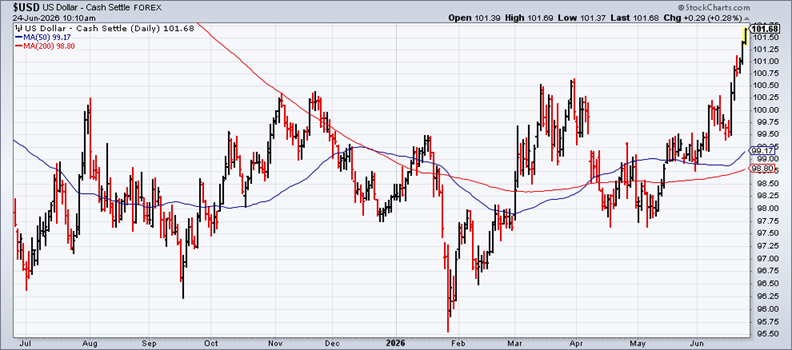

Dollar strength is a key driver of the weakness in foreign bonds. All else equal, a stronger greenback translates into lower prices for foreign assets when measured in US dollar terms.

The currency hit has been especially acute lately. The US Dollar Index—a basket of major currencies—climbed to a 13‑month high on Tuesday (Jun. 23).

Several forces are pushing the dollar higher. One is its lingering safe‑haven appeal. Despite its ups and downs in recent years, the Dollar Index’s rise since the war began suggests investors still view the currency as a refuge in times of geopolitical uncertainty.

Adding to the dollar’s appeal is the expectation that hotter inflation will persuade the Federal Reserve to raise interest rates, boosting the attractiveness of U.S. dollar cash equivalents.

Bank of America expects rate hikes ahead, projecting the current 3.50%–3.75% Fed funds target range will rise to 4.25%–4.50% by year‑end. Supporting the bank’s outlook: nine of the 18 FOMC members anticipate at least one rate increase in 2026, and Fed Chair Kevin Warsh’s hawkish tone at his debut press conference last week.

Christopher Hodge, chief US economist at Natixis, wrote that Warsh “was unambiguously hawkish and doubled down on the notion that ‘inflation is a choice.’ It is clear that inflation will be the focus for the Fed in the near term and that plenty of changes to process, analysis, and communication are afoot.”

Until markets are convinced that inflation risk is contained, relief for bonds—both in the US and abroad—will remain fragile.